Navigating the world of mortgage loans can be both exciting and overwhelming. Whether you’re a first-time homebuyer or looking to refinance your existing mortgage, understanding the ins and outs of mortgage loans is crucial to making informed decisions. This comprehensive guide aims to provide you with a clear understanding of what mortgage loans are, the different types available, eligibility requirements, and the application process.

A mortgage loan is a financial tool that allows individuals and businesses to purchase real estate by borrowing money from a lender. The property being purchased serves as collateral for the loan, providing security for the lender. Mortgage loans come in various forms, each with its own features and suitability for different borrowers. From conventional mortgages to government-backed loans like FHA and VA loans, there are options to meet diverse needs and financial situations.

Mortgage or Mortgage Loan:

A mortgage, also known as a mortgage loan, is a type of loan provided by a financial institution, such as a bank or a lender, to help individuals or businesses purchase real estate. It is a legal agreement where the borrower (the person seeking the loan) pledges the property as collateral to secure the loan. In simpler terms, a mortgage is a loan that allows you to buy a property by borrowing money against the value of that property.

Types of Mortgage Loans:

There are various types of mortgage loans available, and they differ based on factors such as interest rates, repayment terms, and eligibility criteria. Some common types of mortgage loans include:

- Conventional Mortgage: This is a standard mortgage loan offered by banks or lenders, typically requiring a down payment of at least 20% of the property’s purchase price.

- Fixed-Rate Mortgage: In this type of mortgage, the interest rate remains fixed throughout the loan term, which is usually 15 or 30 years. This provides stability in monthly payments.

- Adjustable-Rate Mortgage (ARM): With an ARM, the interest rate is initially fixed for a specific period (e.g., 5 years) and then adjusts periodically based on market conditions. This can result in changing monthly payments.

- FHA Loan: The Federal Housing Administration (FHA) provides mortgage loans that are insured by the government. These loans often have more flexible credit requirements and lower down payment options.

- VA Loan: The U.S. Department of Veterans Affairs (VA) offers mortgage loans exclusively to eligible veterans, active-duty service members, and surviving spouses. VA loans often have favorable terms and require no or low down payments.

- Jumbo Loan: A jumbo loan is a mortgage that exceeds the loan limits set by government-sponsored enterprises like Fannie Mae and Freddie Mac. These loans are typically used for high-value properties.

Can I Get a Mortgage?

Your eligibility for a mortgage depends on several factors, including your credit score, income, employment history, debt-to-income ratio, and the property’s value. Lenders evaluate these factors to assess your ability to repay the loan. Meeting the lender’s criteria and having a favorable financial profile increase your chances of getting approved for a mortgage.

How to Apply for a Mortgage?

To apply for a mortgage, you typically follow these steps:

- Determine your budget: Assess your financial situation and determine how much you can afford to borrow and repay based on your income, expenses, and down payment savings.

- Research lenders: Explore different lenders, such as banks, credit unions, and online lenders, to find competitive mortgage rates and favorable terms.

- Gather documentation: Prepare the necessary documents, including proof of income, tax returns, bank statements, identification, and employment history. Lenders require these documents to evaluate your financial stability.

- Get pre-approved: Consider getting pre-approved for a mortgage. This involves providing your financial information to a lender, who will then give you an estimate of the loan amount you may qualify for. Pre-approval can strengthen your position when making an offer on a property.

- Choose a mortgage type: Based on your research and financial goals, select the type of mortgage loan that best suits your needs.

- Submit the application: Complete the lender’s application form and submit it along with the required documentation. Be prepared to pay an application fee.

- Await approval and loan processing: The lender will review your application, perform a credit check, and assess the property’s value through an appraisal. This process may take some time.

- Loan approval and closing: If your application is approved, the lender will provide a loan commitment letter specifying the terms and conditions. You’ll then proceed to the closing stage, where you’ll sign the loan documents and complete the purchase of the property.

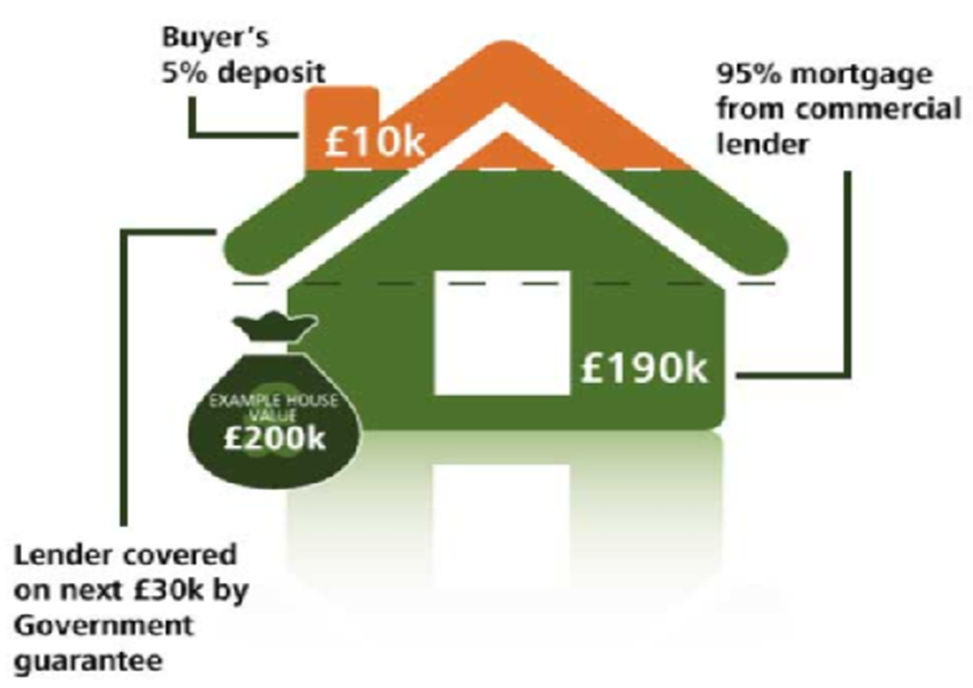

How to Apply for a Government Mortgage Guarantee Scheme:

The process for applying for a government mortgage guarantee scheme may vary depending on the specific program available in your country. However, here are some general steps to follow:

- Research government programs: Explore the government mortgage guarantee schemes offered in your country. Understand the eligibility criteria, loan limits, and other requirements associated with each program.

- Choose a participating lender: Identify lenders that participate in the government mortgage guarantee scheme. These lenders are approved to offer loans under the program.

- Gather documentation: Prepare the necessary documents, such as identification, income proof, bank statements, and any specific documents required by the program.

- Apply through a participating lender: Submit your mortgage application directly to a lender participating in the government scheme. They will guide you through the application process and provide further instructions.

- Await approval and processing: The lender will review your application and assess your eligibility for the government mortgage guarantee scheme. They will also evaluate your financial stability and conduct other necessary checks.

- Complete the process: If approved, you will proceed with the loan closing and follow the lender’s instructions to finalize the mortgage process. Be sure to understand the terms and conditions of the government guarantee and how it affects your loan.

How to Qualify for a Mortgage:

To qualify for a mortgage, lenders typically consider the following factors:

Credit score: A good credit score improves your chances of qualifying for a mortgage. Lenders assess your creditworthiness and history to determine the risk associated with lending you money.

Income and employment history: Lenders evaluate your income stability and employment history to ensure you have a reliable source of income to repay the mortgage.

Debt-to-income ratio (DTI): Your DTI ratio compares your monthly debt payments to your gross monthly income. Lenders prefer borrowers with a lower DTI ratio, as it indicates a lower risk of defaulting on the loan.

Down payment: Most lenders require a down payment, typically a percentage of the property’s purchase price. A larger down payment can increase your chances of mortgage approval.

Property value: Lenders assess the value of the property you intend to purchase, as it serves as collateral for the loan. They want to ensure the property’s value justifies the loan amount.

How Big Mortgage Can I Get?

- The amount of mortgage you can get depends on several factors, including your income, creditworthiness, debt-to-income ratio, and the property’s value. Lenders typically use a formula to determine the maximum loan amount you can qualify for based on your financial profile. This formula takes into account factors like your income, monthly debts, and the loan-to-value ratio (LTV).

- To get an estimate of how big a mortgage you can get, you can use online mortgage calculators provided by lenders or financial institutions. These calculators consider your income, expenses, down payment amount, and interest rates to provide an approximate loan amount you may be eligible for.

- However, it’s important to note that the maximum mortgage amount a lender approves may not always be the best choice for your financial well-being. It’s crucial to consider your budget, monthly repayment capacity, and long-term financial goals when determining how big a mortgage you can comfortably manage.

Frequently Asked Questions

Q.1: What is a mortgage loan?

- A: A mortgage loan is a type of loan provided by a lender to help individuals or businesses purchase real estate, with the property serving as collateral.

Q.2: What types of mortgage loans are available?

- A: There are various types, including conventional mortgages, fixed-rate mortgages, adjustable-rate mortgages (ARM), FHA loans, VA loans, and jumbo loans.

Q.3: How do I qualify for a mortgage loan?

- A: Lenders consider factors such as credit score, income, employment history, debt-to-income ratio, and the property’s value when evaluating mortgage loan applications.

Q.4: How do I apply for a mortgage loan?

- A: To apply, you typically need to research lenders, gather necessary documents (proof of income, tax returns, etc.), complete an application, and submit it to the lender.

Q.5: Can I get a mortgage loan with bad credit?

- A: It may be more challenging, but there are options available. FHA loans, for example, often have more lenient credit requirements.

Q.6: What is a down payment, and how much do I need?

- A: A down payment is a portion of the property’s purchase price paid upfront. The amount required varies but is typically between 3% and 20% of the purchase price.

Q.7: What is a pre-approval for a mortgage loan?

- A: Pre-approval involves providing your financial information to a lender who will estimate the loan amount you may qualify for. It can strengthen your position when making an offer on a property.

Q.8: What is a mortgage interest rate?

- A: The mortgage interest rate is the percentage of the loan amount charged by the lender as interest. It affects your monthly mortgage payment.

Q.9: What is a mortgage term?

- A: The mortgage term is the length of time you have to repay the loan. Common terms are 15 or 30 years, but other options are available.

Q.10: What is private mortgage insurance (PMI)?

- A: PMI is typically required for conventional loans with a down payment of less than 20%. It protects the lender in case the borrower defaults on the loan.

Q.11: Can I refinance my mortgage?

- A: Yes, mortgage refinancing allows you to replace your current mortgage with a new one, often to secure a lower interest rate, change loan terms, or access equity.

Q.12: What are closing costs?

- A: Closing costs are fees and expenses incurred during the mortgage loan closing process, including appraisal fees, title insurance, attorney fees, and more.

Q.13: What happens if I miss a mortgage payment?

- A: If you miss a mortgage payment, it can negatively impact your credit score and result in late fees. Continuous non-payment can lead to foreclosure.

Q.14: Can I pay off my mortgage early?

- A: Yes, it’s possible to pay off your mortgage early by making additional principal payments or by refinancing to a shorter-term loan.

Q.15: What is a mortgage amortization schedule?

- A: A mortgage amortization schedule shows the breakdown of each mortgage payment, indicating how much goes toward principal and interest over the loan term.

Conclusion

In conclusion, a mortgage or mortgage loan is a financial tool that allows individuals and businesses to purchase real estate by borrowing money from a lender, with the property serving as collateral. There are different types of mortgage loans available, including conventional mortgages, fixed-rate mortgages, adjustable-rate mortgages, FHA loans, VA loans, and jumbo loans, each with its own features and eligibility requirements.

When considering whether you can get a mortgage, factors such as your credit score, income, employment history, and the property’s value are taken into account by lenders. To apply for a mortgage, you typically need to determine your budget, research lenders, gather necessary documentation, and submit an application.

[…] Are you dreaming of owning a home in the UK? One of the most important steps in this journey is obtaining a mortgage. Mortgages provide individuals and families with the financial means to purchase a property while spreading the payments over an extended period. Please check out our previous Blog!! […]