Discover how to determine the mortgage amount you can obtain in the UK. This comprehensive guide provides step-by-step instructions, helpful tips, and factors to consider when calculating your borrowing capacity. Start your journey towards homeownership today.

Introduction:

Owning a home is a significant milestone, and determining the mortgage amount you can get is a crucial step towards realizing your dream. This comprehensive guide will take you through the process of calculating the mortgage you can obtain in the UK. By understanding mortgage affordability, evaluating your income and expenses, considering debt-to-income and loan-to-value ratios, factoring in interest rates, seeking professional advice, utilizing online calculators, and preparing the necessary documentation, you’ll be equipped to determine a realistic mortgage amount within your financial capacity. Let’s dive in!

Understanding Mortgage Affordability:

To accurately calculate the mortgage you can get, it’s essential to assess your affordability. Mortgage affordability is determined by various factors, including your income, expenses, and financial stability. By understanding these key elements, you can determine a mortgage amount that aligns with your financial situation.

Evaluating Your Income:

When calculating your mortgage capacity, evaluating your income is a crucial step. Understand the difference between gross and net income, identify stable income sources, and account for any variable income or bonuses you may receive.

Assessing Your Expenses:

To determine your mortgage affordability, it’s important to assess your expenses thoroughly. Identify essential monthly expenses, consider your existing debt obligations and financial commitments, and estimate future expenses related to homeownership.

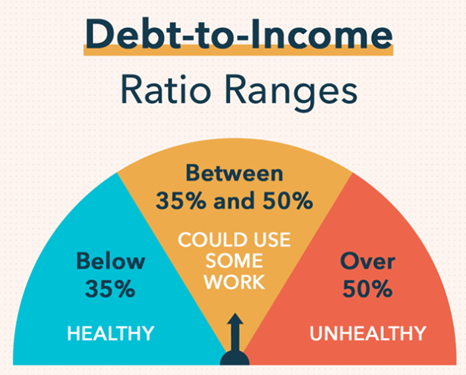

Debt-to-Income Ratio:

The debt-to-income ratio is a significant factor in mortgage approval. Learn how to calculate your debt-to-income ratio and understand the acceptable range for mortgage qualification. Maintaining a healthy debt-to-income ratio increases your chances of securing a mortgage.

Loan-to-Value Ratio:

The loan-to-value ratio is another critical aspect of mortgage calculation. Discover how to calculate your loan-to-value ratio, which represents the loan amount as a percentage of the property’s value. Understanding acceptable loan-to-value ratios helps you gauge your borrowing capacity.

Consideration of Interest Rates:

Interest rates play a vital role in determining your mortgage affordability. Evaluate current interest rates and project their potential impact on mortgage payments. Keeping an eye on interest rate trends helps you make informed decisions.

Consultation with Mortgage Lenders or Brokers:

Seeking professional advice is crucial in the mortgage calculation process. Consult with mortgage lenders or brokers who can provide personalized guidance, explain different mortgage options, and help you understand the specific criteria and requirements of lenders.

Using Online Mortgage Calculators:

Online mortgage calculators are powerful tools that assist in determining your borrowing capacity. Explore the benefits of using online calculators and discover different types available. Learn how to input relevant information accurately to obtain reliable results.

Preparing Required Documentation:

When applying for a mortgage, proper documentation is essential. Gather all necessary documents, ensuring accuracy and completeness. Understand the role of documentation in the mortgage approval process and the importance of providing the required paperwork.

Finalizing Your Mortgage Amount:

Review your calculations and financial capacity to finalize the mortgage amount you can obtain. Consider down payment and deposit requirements, and seek pre-approval for a mortgage to enhance your homebuying journey.

Conclusion:

In conclusion, determining your mortgage capacity is a crucial step towards achieving your goal of homeownership. By understanding the factors that influence mortgage eligibility, assessing your income and expenses, calculating key ratios, considering interest rates, consulting with professionals, utilizing online mortgage calculators, and preparing the necessary documentation, you can navigate the mortgage application process with confidence.

Remember, the information provided in this comprehensive guide serves as a valuable resource, but it’s always advisable to consult with mortgage professionals to obtain personalized advice based on your specific circumstances. By taking proactive steps to determine your mortgage capacity, you can embark on your homeownership journey with clarity and make informed decisions along the way. Start exploring your options today and take the first step towards making your dream of owning a home a reality.

Q.1. How do I determine my mortgage affordability?

Ans. Mortgage affordability is determined by evaluating your income, expenses, debt-to-income ratio, and loan-to-value ratio. By assessing these factors, you can determine a realistic mortgage amount within your financial capacity.

Q.2. What is the debt-to-income ratio, and how is it calculated?

Ans. The debt-to-income ratio is a measure of your monthly debt payments relative to your gross monthly income. To calculate it, add up all your monthly debt payments (such as credit card payments, loan payments, and other obligations) and divide that by your gross monthly income. Multiply the result by 100 to get a percentage. Lenders typically look for a debt-to-income ratio below a certain threshold, such as 43%, but this can vary.

Q.3. How do interest rates affect my mortgage amount?

Ans. Interest rates have a significant impact on your mortgage amount. Higher interest rates mean higher monthly mortgage payments, which can reduce the amount you can borrow. Conversely, lower interest rates can increase your borrowing capacity as they result in more affordable monthly payments.

Q.4. Is it necessary to consult with mortgage lenders or brokers?

Ans. Consulting with mortgage lenders or brokers is highly recommended. They have in-depth knowledge of the mortgage market and can guide you through the process. Lenders can provide information on the specific mortgage options they offer, while brokers have access to multiple lenders and can help you find the best deal based on your needs and financial situation.

Q.5. How accurate are online mortgage calculators?

Ans. Online mortgage calculators provide estimates based on the information you input, making them a useful tool for initial calculations. However, keep in mind that they are only as accurate as the data provided. For a precise assessment, it’s recommended to consult with a mortgage professional who can consider additional factors and provide personalized advice.

Q.6. What documents are required for a mortgage application?

Ans. Required documents may include proof of income (such as pay stubs, tax returns, and employment letters), bank statements, identification documents, proof of assets and liabilities, and information about the property being purchased. Lenders may have specific document requirements, so it’s important to check with them for a complete list.

Q.7. How long does it take to get a mortgage pre-approval?

Ans. The timeframe for mortgage pre-approval can vary. It generally takes a few days to a couple of weeks, depending on factors such as the complexity of your financial situation, the lender’s processes, and the promptness of document submission. Starting the pre-approval process early can help ensure a smoother homebuying journey.

Q.8. Can I make changes to my mortgage amount after pre-approval?

Ans. Yes, you can make changes to your mortgage amount after pre-approval, provided it falls within your financial capacity and the lender’s guidelines. However, it’s important to communicate any changes to your lender and go through the necessary reassessment and approval processes.

Q.9. What is the role of a mortgage broker?

Ans. A mortgage broker acts as an intermediary between you and potential lenders. They have access to a variety of mortgage products and can help you find the best options based on your financial situation and requirements. Brokers assist with the application process, gather necessary documentation, and negotiate terms on your behalf.

Q.10. What should I do after determining my mortgage amount?

Ans. After calculating your mortgage amount, you can take the next steps towards homeownership. Consider saving for a down payment, continue to maintain good credit, gather the required documentation, and consult with lenders or brokers to explore mortgage options and start the application process.

Q.11. How does my income affect my mortgage capacity?

Ans. Your income plays a crucial role in determining your mortgage capacity. Lenders

evaluate your income to assess your ability to make monthly mortgage payments. Higher income generally allows for a higher mortgage amount, but other factors like expenses and debts also come into play.

Q.12. How do interest rates impact my mortgage capacity?

Ans. Interest rates directly affect your mortgage capacity. Lower interest rates result in lower monthly payments, which can increase your borrowing capacity. Conversely, higher interest rates can reduce your mortgage capacity as they lead to higher monthly payments.

Q.13. What factors affect mortgage eligibility?

Ans. Several factors influence mortgage eligibility, including credit score, income, employment history, debt-to-income ratio, loan-to-value ratio, and the property itself. Lenders consider these factors to assess your ability to repay the mortgage.

Q.14. Can I include bonuses and overtime pay when calculating my income for a mortgage?

Yes, you can include bonuses and overtime pay when calculating your income for a mortgage. However, it’s essential to have a consistent history of receiving these additional earnings to provide reassurance to lenders.

Q.15. Does a larger down payment guarantee a higher mortgage amount?

While a larger down payment can increase your chances of qualifying for a mortgage, it does not necessarily guarantee a higher loan amount. Lenders consider various factors, including your income, credit score, and debt-to-income ratio, to determine your borrowing capacity.

Q.16. What is private mortgage insurance (PMI), and how does it impact my mortgage amount?

Private mortgage insurance (PMI) is a type of insurance that protects the lender in case the borrower defaults on the loan. If your down payment is less than 20% of the home’s purchase price, you may be required to pay PMI. This additional cost reduces the overall mortgage amount you can afford.

Q.16. Will paying off my debts improve my chances of getting a higher mortgage?

Paying off your debts or reducing your monthly expenses can improve your debt-to-income ratio (DTI), making you more attractive to lenders. By reducing your DTI, you increase your chances of getting approved for a higher mortgage amount.

Q.17. Can I apply for a mortgage with a low credit score?

While it’s possible to apply for a mortgage with a low credit score, it may be more challenging to secure favorable loan terms. A higher credit score demonstrates your ability to manage debt responsibly and increases your chances of obtaining a larger mortgage.

Leave a Reply