“Discover the formula for calculating monthly UK mortgage payments. Learn about the components of a mortgage, including loan amount, interest rate, and loan term. Understand the factors that can affect your monthly payment. Find answers to FAQs and make informed decisions about your home financing. Get access now to learn more”.

Owning a home is a dream for many individuals, and in the United Kingdom, securing a mortgage is a common way to make this dream a reality. However, understanding how mortgage payments are calculated can be daunting for first-time homebuyers. In this article, we will delve into the formula used to calculate monthly UK mortgage payments, providing a clear understanding of the process.

Table of Contents

- What is a Mortgage?

- The Components of a Mortgage

- Interest Rate and APR

- Loan Term

- Loan Amount

- Monthly Mortgage Payment Formula

- Example Calculation

- Factors Affecting Monthly Mortgage Payments

- Types of Mortgages in the UK

- Fixed-Rate Mortgages

- Variable-Rate Mortgages

- Offset Mortgages

- Repayment vs. Interest-Only Mortgages

- Additional Costs Associated with Mortgages

- FAQs

- Conclusion

1. What is a Mortgage?

A mortgage is a loan provided by a financial institution, such as a bank or building society, to help individuals purchase a property. The loan is secured against the property, which means that if the borrower fails to make the required payments, the lender has the right to repossess the property.

2. The Components of a Mortgage:

To understand the formula for calculating monthly UK mortgage payments, it’s essential to be familiar with the key components of a mortgage:

- Loan Amount: The total amount borrowed to purchase the property.

- Interest Rate: The annual rate at which interest is charged on the loan.

- Loan Term: The length of time over which the mortgage will be repaid.

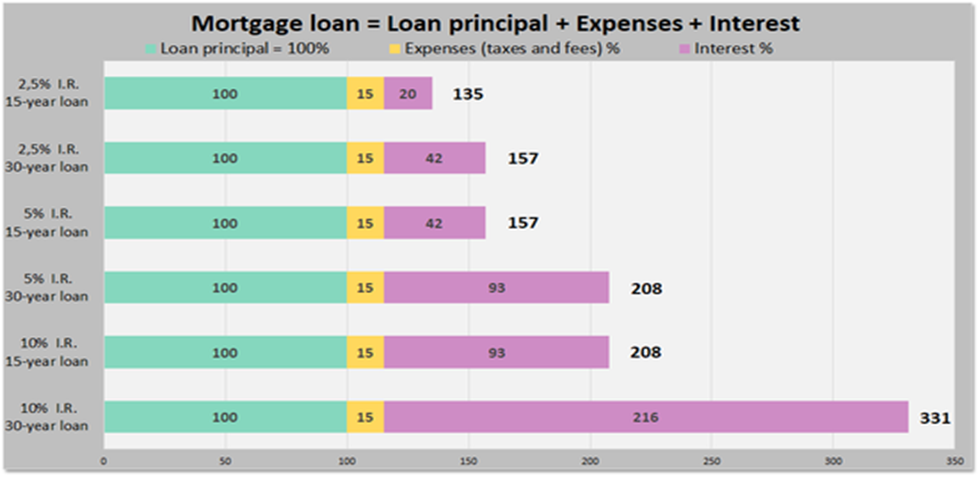

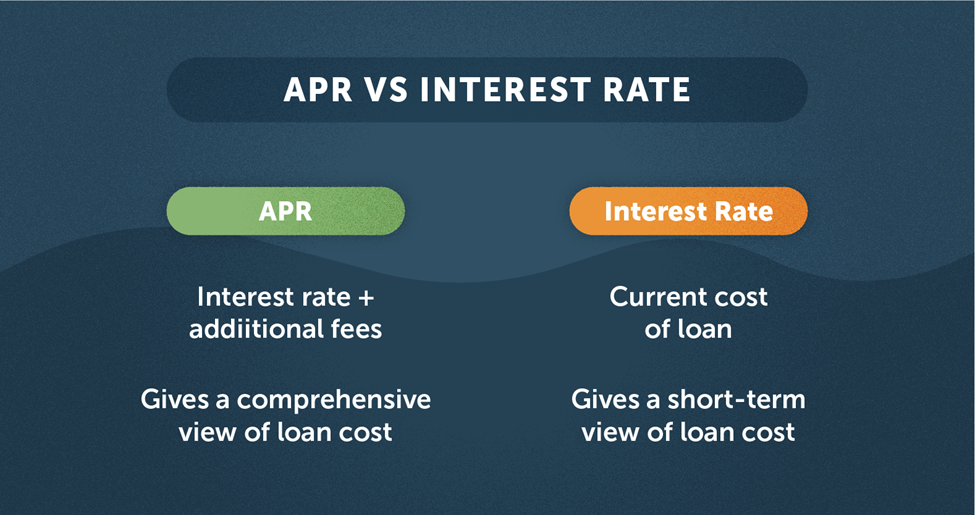

3. Interest Rate and APR

The interest rate is a crucial factor that determines the cost of borrowing. It represents the percentage of the loan amount that the borrower must pay in interest each year. However, it’s important to note that the interest rate alone doesn’t give a complete picture of the overall cost of the mortgage.

The Annual Percentage Rate (APR) provides a more comprehensive view as it includes both the interest rate and any additional fees or charges associated with the mortgage. When comparing different mortgage offers, it’s advisable to consider the APR to understand the true cost of borrowing.

4. Loan Term

The loan term refers to the length of time the borrower has to repay the mortgage. In the UK, mortgage terms typically range from 15 to 30 years, although shorter or longer terms may be available depending on the lender.

The loan term directly affects the monthly mortgage payment. Generally, a shorter loan term will result in higher monthly payments but lower overall interest costs, while a longer loan term will lead to lower monthly payments but higher interest costs over the life of the mortgage.

5. Loan Amount

The loan amount is the total sum borrowed to purchase the property. This includes the purchase price of the property, minus any down payment or deposit made by the borrower. The loan amount, along with the interest rate and loan term, influences the monthly mortgage payment.

6. Monthly Mortgage Payment Formula

The monthly mortgage payment (PMT) can be calculated using the following equation:

- PMT = (P * r * (1 + r)^n) / ((1 + r)^n – 1)

Where:

- PMT is the monthly mortgage payment

- P is the principal amount

- r is the monthly interest rate

- n is the total number of payments

Example Calculation

Suppose you have taken out a mortgage of £200,000 with an annual interest rate of 3.5%. The loan term is 25 years, which amounts to 300 monthly payments.

Using the formula mentioned earlier, we can calculate the monthly mortgage payment as follows:

- P = £200,000

- r = 3.5% / 12 (monthly interest rate)

- n = 300

- PMT = (£200,000 * (0.035/12) * (1 + (0.035/12))^300) / ((1 + (0.035/12))^300 – 1)

By performing the calculations, we find that the monthly mortgage payment would be approximately £988.88.

7. Offset Mortgages

An offset mortgage is a type of mortgage that allows borrowers to link their savings or current accounts to their mortgage. The balance in these accounts is then offset against the outstanding mortgage debt, reducing the interest charged on the mortgage. Offset mortgages can help borrowers save on interest payments and potentially repay their mortgage faster.

8. Repayment vs. Interest-Only Mortgages

When it comes to mortgage repayment, borrowers have the option to choose between a repayment mortgage and an interest-only mortgage.

- Repayment Mortgage: With a repayment mortgage, each monthly payment includes both interest and a portion of the principal loan amount. Over time, the borrower gradually reduces the outstanding balance until the mortgage is fully repaid by the end of the term.

- Interest-Only Mortgage: With an interest-only mortgage, the monthly payment only covers the interest charged on the loan. The borrower is responsible for repaying the principal amount separately. This type of mortgage requires a solid repayment plan to ensure the loan amount is repaid at the end of the term.

9. Additional Costs Associated with Mortgages

Aside from the monthly mortgage payment, there are other costs associated with obtaining and maintaining a mortgage in the UK. Some common additional costs include:

10. Mortgage arrangement or application fees

- Valuation fees

- Legal fees

- Stamp duty (a tax on property purchases)

- Insurance premiums (e.g., buildings insurance, mortgage protection insurance)

It’s important for potential homebuyers to factor in these additional costs when budgeting for a mortgage.

11. FAQ’s (Frequently Asked Questions)

Q.1. Can I calculate my monthly mortgage payment using an online mortgage calculator?

- Yes, many online mortgage calculators are available that can help you estimate your monthly mortgage payment based on the loan amount, interest rate, and loan term.

Q.2. Are there any other factors that can affect my monthly mortgage payment?

- Yes, factors such as property taxes, insurance premiums, and any changes in interest rates can also impact your monthly mortgage payment.

Q.3. What happens if I miss a mortgage payment?

- Missing a mortgage payment can have serious consequences, including late fees, negative impact on credit scores, and the risk of foreclosure. It’s important to contact your lender if you’re facing difficulties in making a payment.

Q.4. Can I pay off my mortgage early?

- Yes, many mortgage agreements allow for early repayment. However, it’s important to review the terms of your mortgage and any associated fees or penalties for early repayment.

Q.5. Should I consider remortgaging?

- Remortgaging, or refinancing, can be beneficial if it allows you to secure a lower interest rate or better loan terms. It’s advisable to speak with a mortgage advisor to evaluate whether remortgaging is the right option for you.

Q.6. What is a mortgage deposit, and how does it affect my monthly payment?

- A mortgage deposit is the initial amount of money you contribute towards the purchase price of a property. The size of your deposit can impact your monthly mortgage payment. A larger deposit reduces the loan amount, resulting in a lower monthly payment and potentially better interest rates.

Q.7. What is a mortgage agreement in principle, and should I obtain one?

- A mortgage agreement in principle, also known as a decision in principle or mortgage pre-approval, is a preliminary assessment by a lender to determine the amount they may be willing to lend you. Obtaining one can be beneficial as it gives you an idea of your borrowing capacity and helps you in property search and negotiations.

Q.8. Can I switch my mortgage to a different lender?

- Yes, it is possible to switch your mortgage to a different lender. This is known as remortgaging. Before making a switch, consider any associated costs, such as early repayment fees and legal fees, and compare the new offer with your current mortgage to ensure it is financially advantageous.

Q.9. What is an overpayment on a mortgage, and can it reduce my monthly payment?

- An overpayment is when you make additional payments towards your mortgage, reducing the outstanding balance. While overpayments can save you interest and help you pay off your mortgage faster, they typically don’t reduce your monthly payment. Instead, they shorten the overall term of your mortgage.

Q.10. Can I make changes to my mortgage term after taking out the loan?

- It is possible to make changes to your mortgage term after taking out the loan, but it depends on your lender’s policies. Some lenders allow you to extend or shorten the term, while others may impose limitations or fees for such changes. Contact your lender to discuss the available options.

Q.11. How does my credit score affect my ability to secure a mortgage?

- Your credit score plays a significant role in determining your eligibility for a mortgage. Lenders use it to assess your creditworthiness and evaluate the risk of lending to you. A higher credit score generally improves your chances of obtaining a mortgage and may result in more favorable interest rates.

Q.12. What is a mortgage affordability assessment, and why is it important?

- A mortgage affordability assessment is an evaluation of your financial situation, including income, expenses, and debt, to determine the amount of mortgage you can afford. It is crucial to undergo this assessment to ensure you don’t overextend yourself financially and can comfortably meet the monthly mortgage payments.

Q.13. Are there any government schemes or programs to assist first-time buyers?

- Yes, there are several government schemes and programs aimed at assisting first-time buyers, such as Help to Buy, Shared Ownership, and the Lifetime ISA. These schemes offer various forms of financial support, including shared equity loans, shared ownership arrangements, and government bonuses on savings.

Q.14. What is the difference between a mortgage broker and a mortgage lender?

- A mortgage broker acts as an intermediary between borrowers and lenders, helping borrowers find the most suitable mortgage products from a range of lenders. A mortgage lender, on the other hand, is the financial institution that provides the funds for your mortgage. Both play important roles in the mortgage process.

Q.15. Can I get a mortgage if I am self-employed or have irregular income?

- Yes, it is possible to obtain a mortgage if you are self-employed or have irregular income. However, lenders typically require additional documentation, such as tax returns or business accounts, to assess your income stability and affordability. Working with a mortgage broker experienced in such cases can be beneficial.

Conclusion

Understanding how monthly UK mortgage payments are calculated is crucial for anyone considering buying a property. By knowing the components of a mortgage, the formula used for calculation, and the various factors that can affect the monthly payment, individuals can make informed decisions about their home financing options.

Remember, when seeking a mortgage, it’s essential to consult with mortgage advisors or professionals to ensure you choose the most suitable mortgage product for your needs and financial circumstances.

Leave a Reply