Buying a house is an exciting milestone, but it also involves financial considerations and planning. Understanding how mortgage payments work in the UK is crucial for potential homeowners. This article aims to provide insights into the factors affecting house payments, calculation methods, different types of mortgages, and additional costs to consider. By the end of this article, you’ll have a better understanding of what your house payment in the UK might look like and how to plan for it.

1. Introduction

Purchasing a house often requires financing through a mortgage. A mortgage is a loan provided by a bank or lender specifically for purchasing a property. Repaying the mortgage involves making regular payments, typically on a monthly basis, to cover both the principal amount borrowed and the interest charged by the lender.

2. How Mortgage Payments Work

Mortgage payments consist of two main components: principal and interest. The principal refers to the initial loan amount borrowed to purchase the property, while the interest is the additional fee charged by the lender for lending the money. These payments are usually spread over a specific period, known as the loan term.

3. Factors Affecting House Payments in the UK

Several factors influence the amount of your house payment in the UK. It’s essential to consider these factors to estimate and plan your monthly payments accurately.

- Interest Rates

Interest rates play a significant role in determining the cost of borrowing money for a mortgage. When interest rates are low, the overall mortgage payments tend to be more affordable. Conversely, high-interest rates can increase the cost of borrowing and subsequently raise the monthly payments.

- Loan Amount

The loan amount, also known as the mortgage principal, is the total sum borrowed to purchase the property. The higher the loan amount, the larger the monthly payments will be. It’s important to evaluate how much you can afford and consider your down payment when determining the loan amount.

- Loan Term

The loan term refers to the duration over which the mortgage will be repaid. Common terms in the UK range from 25 to 30 years, although shorter and longer terms are available. Shorter loan terms typically result in higher monthly payments but enable faster repayment and lower interest charges.

- Credit Score

Your credit score is an important factor that lenders consider when assessing your eligibility for a mortgage. A higher credit score indicates a lower risk for the lender, potentially leading to more favorable interest rates and terms. It’s advisable to maintain a good credit score by paying bills on time and managing debts responsibly.

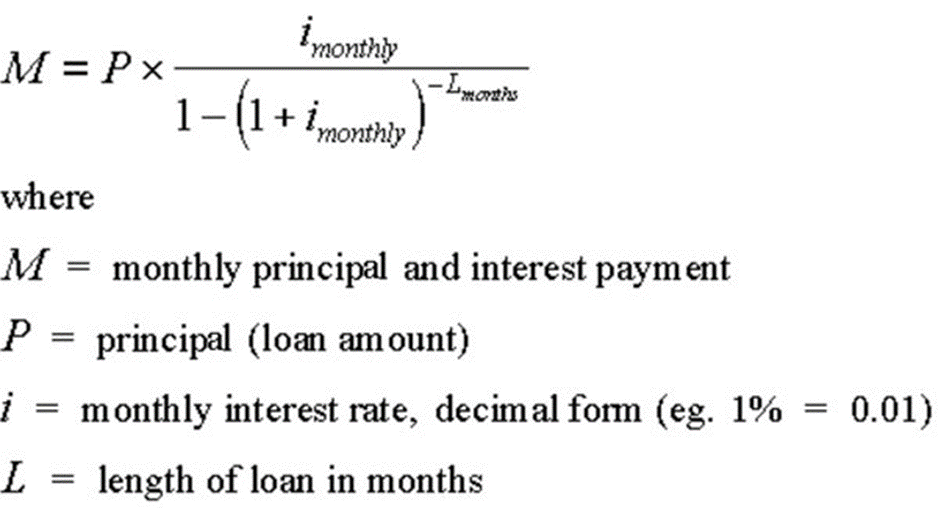

4. Calculating House Payments

Estimating your house payments can be done using various mortgage calculator tools available online. These tools consider the loan amount, interest rate, and loan term to provide an estimate of your monthly payments. Additionally, they may also factor in other costs such as property taxes and insurance.

To give you a clearer understanding, let’s consider an example calculation. Suppose you’re purchasing a property with a mortgage of £200,000, an interest rate of 3.5%, and a loan term of 25 years. Using a mortgage calculator, you can determine that your monthly payment would be approximately £1,003.

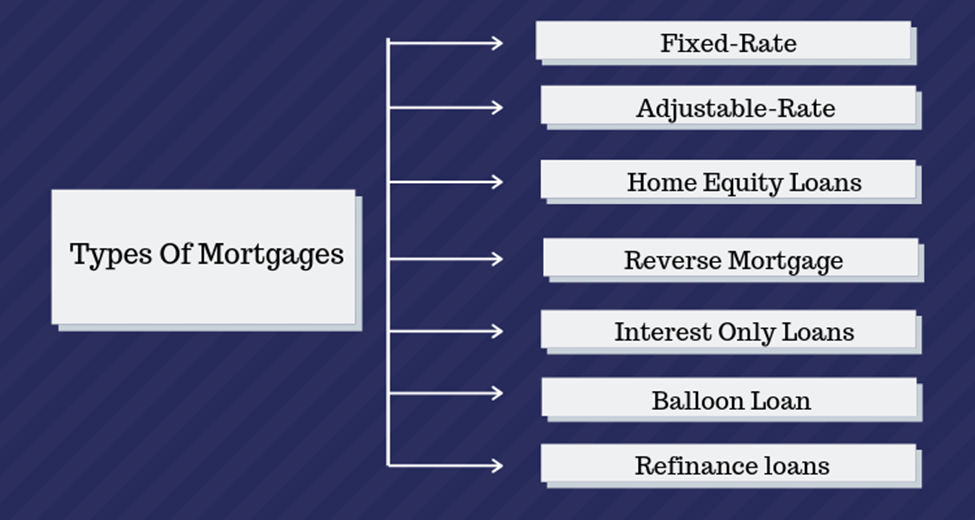

5. Types of Mortgage Payments

In the UK, there are several types of mortgage payments to choose from, each with its own characteristics and considerations. Here are some common types:

- Fixed-Rate Mortgages

With a fixed-rate mortgage, the interest rate remains constant throughout the loan term. This means that your monthly payments will remain unchanged, providing stability and predictability. Fixed-rate mortgages are popular among homeowners who prefer a consistent payment amount over time.

- Adjustable-Rate Mortgages

Unlike fixed-rate mortgages, adjustable-rate mortgages (ARMs) have interest rates that can change periodically. Typically, ARMs offer an initial fixed-rate period, after which the rate adjusts periodically based on market conditions. These mortgages often come with lower initial interest rates but carry the risk of potential rate increases in the future.

- Interest-Only Mortgages

Interest-only mortgages allow borrowers to pay only the interest portion of the loan for a specific period, usually around 5 to 10 years. During this period, the monthly payments are lower, but the principal amount remains unchanged. After the interest-only period ends, borrowers must begin repaying both the principal and the interest, resulting in higher monthly payments.

- Buy-to-Let Mortgages

Buy-to-let mortgages are specifically designed for individuals who want to purchase a property with the intention of renting it out. These mortgages often have different criteria and interest rates compared to traditional residential mortgages. If you’re considering investing in rental properties, it’s essential to explore buy-to-let mortgage options.

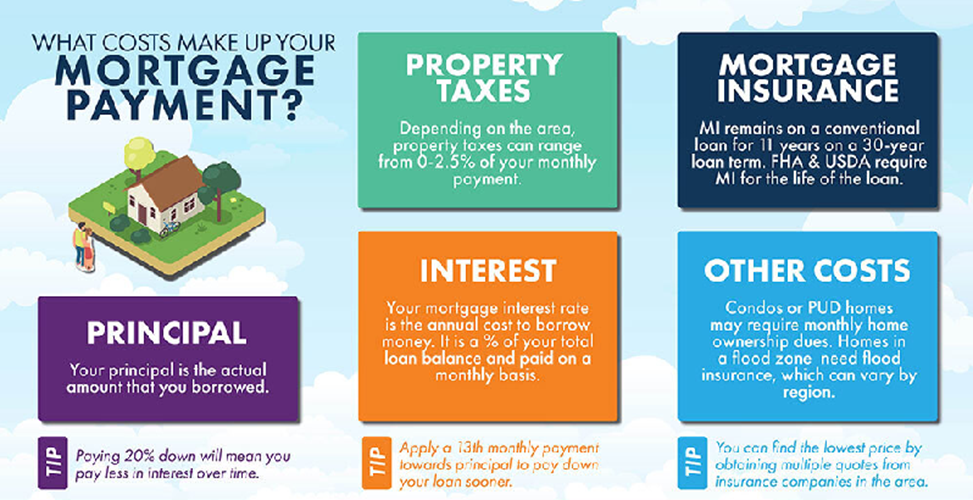

6. Additional Costs and Considerations

When calculating your house payments, it’s crucial to account for additional costs associated with homeownership. These costs can impact your overall budget and affordability. Here are some important factors to consider:

- Property Taxes

Property taxes vary depending on the location and value of your property. These taxes are usually assessed annually and contribute to local government funding. It’s important to research and factor in property tax expenses when estimating your monthly payments.

- Insurance

Homeowner’s insurance is essential for protecting your property against unforeseen events, such as fire, theft, or natural disasters. The cost of insurance can vary depending on factors like the property value, location, and coverage options. Be sure to include insurance costs in your budget.

- Maintenance and Repairs

Owning a home entails regular maintenance and potential repairs. It’s advisable to set aside a portion of your budget for maintenance costs, such as landscaping, repairs, and general upkeep. Properly maintaining your property can help preserve its value in the long run.

- Down Payment

A down payment is the initial payment made towards the property purchase. In the UK, a typical down payment is around 10% to 20% of the property’s value. A larger down payment can lower your loan amount and potentially reduce your monthly payments. It’s important to consider your down payment options and how they align with your financial situation.

7. Affordability and Budgeting

To determine what house payment you can afford in the UK, it’s essential to assess your financial situation and create a realistic budget. Consider the following factors:

- Evaluate your income and expenses: Calculate your monthly income and assess your regular expenses. Deduct your existing financial commitments to determine the amount you can allocate towards your house payment.

- Consider your debt-to-income ratio: Lenders often consider your debt-to-income ratio when approving a mortgage. This ratio compares your monthly debt payments to your monthly income. Aim to keep your debt-to-income ratio within acceptable limits.

- Plan for a contingency fund: It’s prudent to have a contingency fund to cover unexpected expenses or financial emergencies. Set aside a portion of your budget for savings to build a safety net.

- Seek professional advice: If you’re uncertain about affordability or need assistance with budgeting, consider consulting with a financial advisor or mortgage specialist. They can provide personalized guidance based on your circumstances.

By carefully assessing your finances and creating a budget, you can determine a realistic house payment that aligns with your financial goals and capabilities.

8. FAQs (Frequently Asked Questions)

Q1. Can I estimate my mortgage payment without a mortgage calculator?

- Yes, although using a mortgage calculator provides a more accurate estimate, you can make a rough calculation manually. Simply multiply the loan amount by the monthly interest rate and divide it by the number of months in the loan term. Remember to include additional costs such as insurance and taxes.

Q2. What happens if interest rates increase during my adjustable-rate mortgage term?

- If interest rates increase during your adjustable-rate mortgage term, your monthly payments will likely rise accordingly. It’s important to consider this possibility and assess your ability to handle potential payment increases before choosing an ARM.

Q3. Can I negotiate the interest rate with my lender?

- In some cases, you may be able to negotiate the interest rate with your lender. This usually depends on factors such as your credit score, financial stability, and market conditions. It’s worth exploring this option and comparing offers from different lenders.

Q4. How can I improve my credit score to obtain better mortgage terms?

- To improve your credit score, focus on making timely bill payments, reducing existing debts, and maintaining a low credit utilization ratio. Regularly checking your credit report for errors and addressing them promptly can also positively impact your credit score.

Q5. Should I prioritize paying off other debts before applying for a mortgage?

- Paying off high-interest debts and reducing your overall debt burden can improve your financial position and potentially result in better mortgage terms. Evaluate your debts and prioritize them based on interest rates and financial goals.

Q6. How much do I need for a down payment in the UK?

- A: The typical down payment in the UK ranges from 10% to 20% of the property’s value. However, it’s possible to find mortgage options with lower down payment requirements.

Q7. Can I qualify for a mortgage with a low credit score?

- A: While a low credit score may affect your mortgage options, it’s still possible to qualify for a mortgage. Lenders may offer higher interest rates or require a larger down payment. Improving your credit score beforehand can increase your chances of securing a favorable mortgage.

Q8. What is the maximum mortgage term in the UK?

- A: The maximum mortgage term in the UK is typically 35 years. However, shorter loan terms, such as 25 or 30 years, are more common.

Q9. Are there any penalties for paying off a mortgage early?

- A: Some mortgage agreements include early repayment penalties. It’s important to review the terms and conditions of your mortgage contract to understand if such penalties apply.

Q10. How do interest rates impact my mortgage payments?

- A: Higher interest rates result in higher mortgage payments, while lower interest rates lead to more affordable payments. It’s essential to consider interest rate trends and evaluate their potential impact on your monthly payments.

Q11. Can I switch mortgage lenders to get a better interest rate?

- A: Switching mortgage lenders to get a better interest rate is possible. However, it’s important to consider any associated fees, such as exit fees from your current lender and arrangement fees with the new lender, to ensure it’s financially beneficial.

Q12. Can I pay off my mortgage early?

- A: Yes, many mortgages allow for early repayment. However, you should check your specific mortgage terms as some lenders may charge early repayment fees.

Q13. What additional costs should I consider when buying a house?

- A: In addition to the mortgage payment, you should consider costs like property taxes, homeowner’s insurance, maintenance and repairs, and potential fees associated with the home buying process, such as legal fees and survey costs.

Q14. What are the benefits of a fixed-rate mortgage?

- A: A fixed-rate mortgage provides stability as the interest rate remains constant throughout the loan term. This allows for predictable monthly payments, making budgeting easier.

Q15. Can I use gifted money as a down payment for a mortgage?

- A: Some mortgage lenders accept gifted money as a down payment, but they may require documentation to verify the source of the funds and ensure they are a gift and not a loan.

Remember, these answers are for informational purposes only, and it’s advisable to consult with professionals for personalized advice based on your specific circumstances.

9. Conclusion

Understanding mortgage payments is vital for prospective homeowners in the UK. By considering factors such as interest rates, loan amount, loan term, and credit score, you can estimate your monthly payments more accurately. Exploring different types of mortgages and factoring in additional costs like property taxes, insurance, maintenance, and repairs allows for a comprehensive understanding of the overall financial commitment. By carefully planning and budgeting, you can make informed decisions and achieve your goal of homeownership in the UK.

Leave a Reply