“Discover everything you need to know about mortgages in the UK. From types of mortgages to the application process, find expert guidance on securing a mortgage, understanding interest rates, and making informed decisions. Get valuable insights on factors to consider, finding the right lender, and tips for successful mortgage applications. Start your journey to homeownership today.”

In the UK, purchasing a property often involves securing a mortgage. Mortgages provide individuals and families with the means to own a home without paying the full purchase price upfront. This article will explore the ins and outs of mortgages in the UK, including the different types available, the application process, and important considerations for potential borrowers.

What is a Mortgage?

A mortgage is a loan specifically designed for purchasing property. It allows individuals to borrow a large sum of money from a lender, typically a bank or building society, to fund the purchase of a home. The borrower then makes regular repayments over an agreed-upon period, often spanning several years, until the loan is fully repaid.

Types of Mortgages in the UK

There are various types of mortgages available in the UK, each catering to different borrower needs and financial situations. Some common types include:

- Fixed-rate mortgages: These mortgages offer a fixed interest rate for a specific term, providing borrowers with stability and predictable monthly repayments.

- Variable-rate mortgages: With variable-rate mortgages, the interest rate can fluctuate over time, often in line with the Bank of England’s base rate.

- Tracker mortgages: Tracker mortgages are directly linked to the Bank of England’s base rate, with an additional percentage added. This means that if the base rate changes, the borrower’s interest rate will also change accordingly.

- Interest-only mortgages: With an interest-only mortgage, borrowers only pay the interest on the loan each month. The capital must be repaid at the end of the mortgage term.

- Buy-to-let mortgages: Designed for individuals who wish to purchase a property to let it out, buy-to-let mortgages have specific criteria and requirements.

Mortgage process in the UK

Applying for a mortgage in the UK involves several steps:

- Assessing affordability: Potential borrowers should evaluate their financial situation, including income, expenses, and existing debt, to determine how much they can comfortably borrow.

- Researching mortgage lenders: It’s essential to compare different mortgage lenders to find the one that offers favorable rates, terms, and customer service.

- Pre-approval: Some borrowers opt to get pre-approved for a mortgage before house hunting. This helps in understanding the budget and demonstrates to sellers that the buyer is serious.

- Property search: Once pre-approved, borrowers can begin their property search, keeping in mind their budget and requirements.

- Making an offer: When a suitable property is found, the buyer makes an offer, which, if accepted, leads to the next step.

- Mortgage application: The borrower submits a formal mortgage application, providing all necessary documentation, such as proof of income, identification, and property details.

- Mortgage valuation: The lender assesses the property’s value to ensure it’s suitable as collateral for the mortgage.

- Mortgage offer: If the lender approves the application, they issue a mortgage offer, detailing the loan amount, interest rate, and terms.

- Exchange of contracts: Once the buyer and seller have agreed upon the purchase, contracts are exchanged, and a completion date is set.

- Completion: On the completion date, the mortgage funds are transferred to the seller, and legal ownership of the property is transferred to the buyer.

Factors to Consider Before Applying for A Mortgage

Before applying for a mortgage, there are several important factors to consider:

- Affordability: It’s crucial to assess whether the monthly mortgage repayments fit comfortably within the budget.

- Credit score: A good credit score improves the chances of securing a mortgage with favorable terms and interest rates.

- Deposit: The higher the deposit, the better the mortgage options available.

- Employment history: Lenders often prefer borrowers with stable employment and income sources.

- Future plans: Consider long-term plans, such as career growth, family, and potential changes in income, when determining the mortgage term.

Finding the Right Mortgage Lender

Choosing the right mortgage lender is crucial to ensure a smooth borrowing experience. Consider the following when selecting a lender:

- Interest rates: Compare interest rates offered by different lenders and consider whether they are fixed, variable, or tracker rates.

- Fees and charges: Look out for any additional fees or charges associated with the mortgage, such as arrangement fees, valuation fees, or early repayment charges.

- Customer service: Read reviews and gather information about the lender’s reputation for customer service.

- Flexibility: Consider whether the lender offers flexible repayment options, such as overpayments or payment holidays.

- Mortgage advice: Some lenders provide personalized mortgage advice, which can be beneficial, especially for first-time buyers.

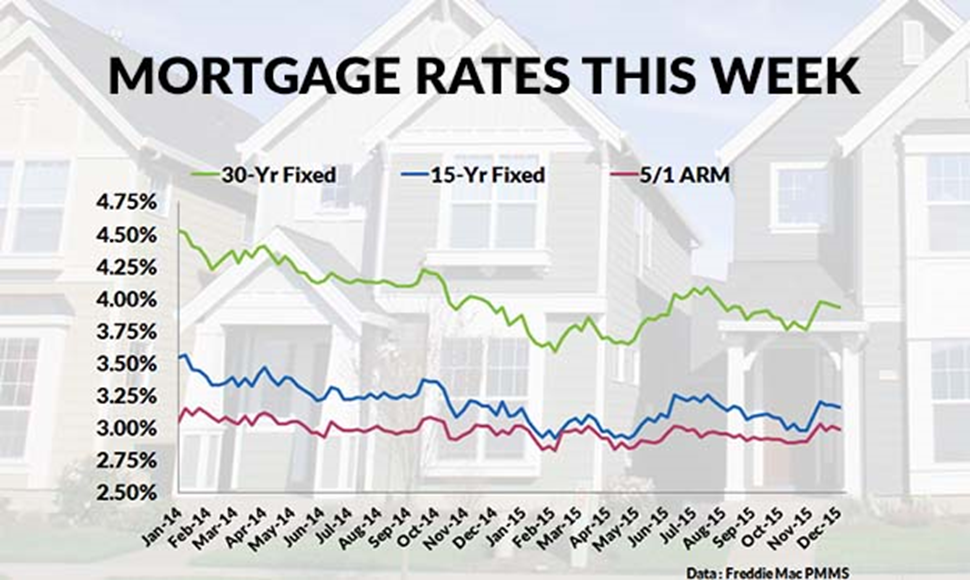

Mortgage Rates and Interest

Mortgage rates in the UK can vary depending on several factors, including the type of mortgage, the borrower’s credit history, the loan-to-value ratio, and the overall economic conditions. It’s important to understand how interest rates can impact monthly repayments and the total cost of the mortgage over its term.

Understanding Mortgage Terms and Conditions

Before committing to a mortgage, it’s essential to carefully review the terms and conditions. Pay attention to details such as early repayment charges, penalties for missed payments, and the consequences of defaulting on the mortgage.

Benefits of Getting a Mortgage in the UK

Obtaining a mortgage in the UK offers several advantages:

- Property ownership: A mortgage allows individuals to become homeowners, providing stability and a sense of security.

- Potential for property value appreciation: Over time, the value of the property may increase, leading to potential financial gains.

- Building equity: As mortgage repayments are made, equity in the property is built, which can be used for future investments or as collateral for other loans.

- Tax benefits: There may be tax advantages associated with mortgage interest payments, such as deductibility from income tax.

Potential Risks and Challenges of Mortgages

While mortgages offer numerous benefits, it’s important to be aware of the risks and challenges involved:

- Financial commitment: Mortgages require long-term financial commitments, and failure to meet repayments could result in repossession of the property.

- Interest rate fluctuations: Variable-rate mortgages are susceptible to changes in interest rates, which can impact monthly repayments.

- Affordability challenges: Changes in personal circumstances, such as job loss or reduced income, may make it difficult to meet mortgage repayments.

- Additional costs: Owning a property comes with additional expenses, such as property maintenance, insurance, and taxes.

Tips for a Successful Mortgage Application

To increase the chances of a successful mortgage application, consider the following tips:

1. Improve credit score

When it comes to applying for a mortgage, having a good credit score can significantly impact your chances of approval and the terms you’re offered. Here are some valuable tips to help you improve your credit score and enhance your prospects of a successful mortgage application:

- Pay bills on time: Late payments can have a negative impact on your credit score. Make it a priority to pay your bills, including credit cards, loans, and utilities, on or before their due dates.

- Reduce credit utilization: Aim to keep your credit card balances low, ideally below 30% of your credit limit. High credit utilization can indicate a reliance on credit and may be seen as a risk by lenders.

- Minimize new credit applications: Every time you apply for credit, it generates a hard inquiry on your credit report, which can temporarily lower your score. Limit new credit applications and only apply for credit when necessary.

- Review your credit report: Regularly check your credit report for errors or inaccuracies that could be dragging down your score. Dispute any incorrect information and ensure your report reflects your current financial situation.

- Maintain a mix of credit: A healthy credit mix, including credit cards, loans, and a mortgage (if applicable), can demonstrate your ability to manage different types of credit responsibly.

- Keep old accounts open: Length of credit history is an important factor in credit scoring. If you have old accounts with positive payment history, keep them open to maintain a longer credit history.

- Avoid closing credit cards: Closing credit card accounts can impact your credit utilization ratio. Instead of closing them, consider keeping them open with minimal or occasional usage to maintain a low credit utilization ratio.

- Set up payment reminders: Missing payments can harm your credit score. Utilize payment reminders, automatic payments, or calendar alerts to ensure you never miss a payment deadline.

- Address outstanding debts: Tackle any outstanding debts systematically. Create a plan to pay off debts, starting with those carrying the highest interest rates or balances.

- Seek professional advice: If you’re struggling with debt or credit issues, consider seeking advice from a reputable credit counseling agency or financial advisor. They can provide tailored guidance to improve your credit and overall financial health.

2. Save for a higher deposit

A larger deposit can increase your chances of getting approved for a mortgage and may also result in better interest rates.

- Organize your financial documents: Gather all the necessary financial documents, such as bank statements, pay stubs, and tax returns, to streamline the application process.

- Minimize credit applications: Avoid making multiple credit applications in a short period, as it can negatively impact your credit score.

- Seek professional advice: Consider consulting with a mortgage advisor who can provide guidance on the application process and help you find suitable mortgage options.

Mortgage Repayment Options

When it comes to mortgage repayments, borrowers typically have different options:

- Repayment mortgages: With a repayment mortgage, borrowers make monthly repayments that cover both the principal amount and the interest. Over time, the loan is gradually paid off.

- Interest-only mortgages: In an interest-only mortgage, borrowers only pay the interest on the loan each month. The principal amount remains unchanged, and a separate plan is needed to repay the capital at the end of the mortgage term.

How to Improve your Chances of getting approved for a Mortgage

To increase the likelihood of mortgage approval, consider the following strategies:

- Improve creditworthiness: Maintain a good credit score by paying bills on time, reducing debt, and rectifying any errors on your credit report.

- Save for a larger deposit: A higher deposit not only improves your chances of approval but can also result in better interest rates and lower monthly repayments.

- Stability in employment: Lenders prefer borrowers with stable employment and a consistent income source. Avoid changing jobs or careers shortly before applying for a mortgage.

- Minimize existing debt: Lenders assess your debt-to-income ratio, so paying off outstanding debt can improve your borrowing capacity.

- Check your affordability: Calculate your monthly income and expenses to determine how much you can comfortably afford to repay each month.

Common Misconceptions About Mortgages

There are several misconceptions surrounding mortgages. Let’s debunk some of the common ones:

- “Renting is always better than owning a property”: While renting offers flexibility, owning a property can provide long-term financial benefits and stability.

- “A large income guarantees mortgage approval”: Lenders assess affordability based on various factors, not just income. Your credit history, debt levels, and deposit also play a significant role.

- “Fixed-rate mortgages are always better than variable-rate mortgages”: The best mortgage type depends on your individual circumstances and preferences. Both options have their advantages and considerations.

FAQs (Frequently Asked Questions)

Q1: What is the minimum deposit required for a mortgage in the UK?

- A: The minimum deposit required for a mortgage in the UK is typically around 5% to 10% of the property’s value. However, a larger deposit can lead to more favorable mortgage terms.

Q2: Are there any government schemes to help first-time buyers?

- A: Yes, the UK government offers various schemes to assist first-time buyers, such as Help to Buy and Shared Ownership, which aim to make homeownership more accessible.

Q3: Can I switch mortgage lenders?

- A: Yes, it is possible to switch mortgage lenders. However, it’s important to consider any exit fees or penalties associated with your existing mortgage before making a decision.

Q4: How long does the mortgage application process take?

- A: The mortgage application process can vary, but on average, it takes around 4-6 weeks. However, it can be longer if there are complex circumstances or delays in obtaining necessary documentation.

Q5: Can self-employed individuals get a mortgage in the UK?

- A: Yes, self-employed individuals can apply for a mortgage in the UK. However, the process may require additional documentation to verify income and affordability.

Q6: Can I get a mortgage with a low credit score?

- A: It can be challenging to get a mortgage with a low credit score, but not impossible. Some lenders specialize in providing mortgages to individuals with less-than-perfect credit. However, you may need to demonstrate other positive factors, such as a larger deposit or stable employment, to improve your chances.

Q7: What is a mortgage agreement in principle?

- A: A mortgage agreement in principle, also known as a mortgage decision in principle or mortgage promise, is a conditional offer from a lender indicating the amount they would be willing to lend you based on an initial assessment of your finances. It can be useful when house hunting to show sellers that you have the potential to secure a mortgage.

Q8: What is the difference between a mortgage broker and a mortgage lender?

- A: A mortgage broker acts as an intermediary between borrowers and multiple lenders, helping to find the most suitable mortgage options based on the borrower’s circumstances. On the other hand, a mortgage lender is the financial institution that provides the funds for the mortgage.

Q9: Can I get a mortgage if I’m self-employed?

- A: Yes, self-employed individuals can get a mortgage in the UK. However, the application process may require additional documentation, such as tax returns and business accounts, to verify income and affordability.

Q10: Can I make overpayments on my mortgage?

- A: Many mortgage agreements allow borrowers to make overpayments, which can help reduce the overall interest paid and potentially shorten the mortgage term. However, it’s important to check your specific mortgage terms and any associated penalties for overpayments.

Q11: What is a mortgage term?

- A: The mortgage term refers to the length of time over which you have agreed to repay the mortgage. Typical mortgage terms in the UK range from 25 to 35 years, although shorter terms are also available.

Q12: Can I port my mortgage to a new property?

- A: Some mortgage agreements offer the option to port the mortgage to a new property when you move home. This means you can transfer the existing mortgage to the new property, potentially avoiding early repayment charges. However, it’s subject to the lender’s approval and specific terms.

Q13: What happens if I miss a mortgage payment?

- A: Missing a mortgage payment can have serious consequences. It may result in late payment fees, damage your credit score, and could ultimately lead to repossession if the issue persists. If you’re struggling to make a payment, it’s essential to contact your lender as soon as possible to discuss potential solutions.

Q14: Can I remortgage my property to release equity?

- A: Remortgaging is a common option for releasing equity from a property. By refinancing your mortgage, you can potentially borrow additional funds based on the increased value of your property. This can be used for various purposes, such as home improvements or debt consolidation.

Q15: What is a mortgage indemnity guarantee?

- A: A mortgage indemnity guarantee, also known as a mortgage indemnity insurance, is a type of insurance that protects the lender against financial loss if the borrower defaults on the mortgage and the property is repossessed. It is typically required when the borrower has a high loan-to-value ratio, such as a small deposit.

Please note that these FAQs provide general information and it’s always advisable to seek personalized advice from a mortgage professional to address your specific circumstances and requirements.

Conclusion

Securing a mortgage in the UK is a significant financial commitment but can provide the opportunity to own a home and build equity. By understanding the types of mortgages available, the application process, and the factors to consider, potential borrowers can navigate the mortgage journey more effectively.

Leave a Reply